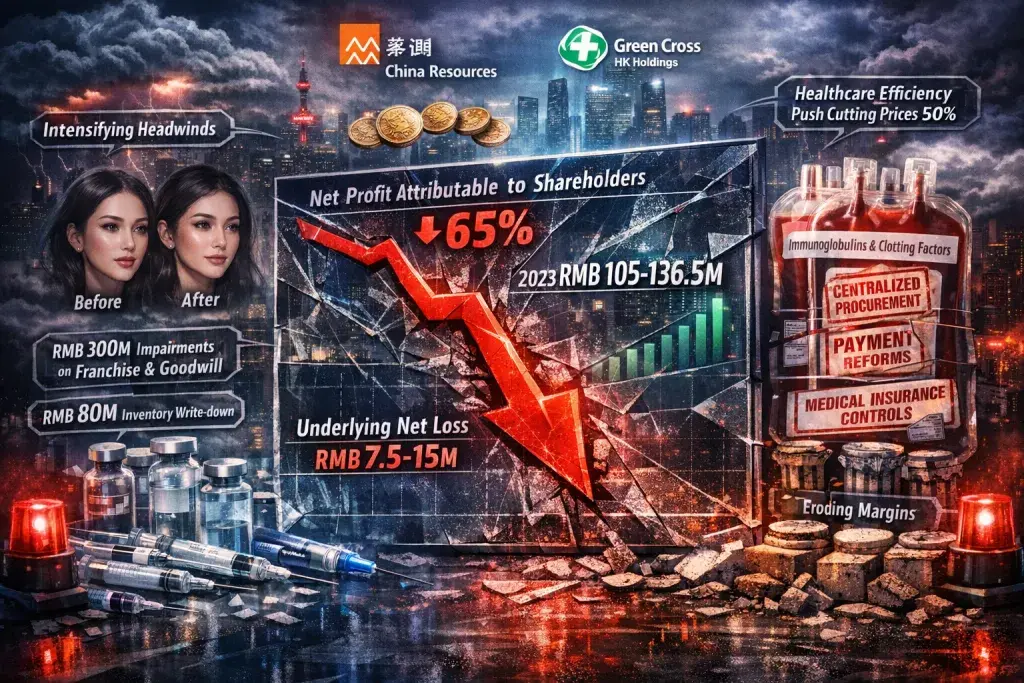

China Resources Boya Bio-pharmaceutical, a key player in biopharmaceuticals, has released a stark profit warning for 2025, forecasting net profit attributable to shareholders at RMB105 million to RMB136.5 million—down over 65% from RMB397 million in the prior year. Stripping out non-recurring gains reveals an underlying net loss of RMB7.5 million to RMB15 million. This alert underscores intensifying headwinds in China's competitive biopharma landscape, where regulatory shifts and market saturation threaten profitability.

Acquisition Drives Impairments Amid Aesthetics Slump

The primary culprit is a downturn in the hyaluronic acid medical aesthetics market, a segment reliant on injectables for dermal fillers and tissue augmentation. Management cites roughly RMB300 million in impairments on franchise rights and goodwill from the November 2024 acquisition of Green Cross HK Holdings, plus RMB80 million in inventory revaluation hits and elevated depreciation.

- Operating revenue still projected to grow 10-25%, fueled by the Green Cross integration.

- Non-recurring gains, like government subsidies and investment income, to contribute about RMB120 million, softening the blow.

Blood Products Face Regulatory and Competitive Pressures

CR Boya's blood products division, a traditional revenue pillar, grapples with China's centralized procurement policies, payment reforms, stricter medical insurance controls, and rising competition. These factors have eroded gross margins, mirroring broader challenges in the plasma-derived therapeutics market where volume-based pricing squeezes profits.

Expert insight reveals how such reforms aim to enhance affordability but often penalize mid-tier players like CR Boya, accelerating consolidation in a sector vital for treatments like immunoglobulins and clotting factors.

Implications for Biopharma and Healthcare Trends

This profit warning signals deeper vulnerabilities for CR Boya and parent China Resources Pharmaceutical, highlighting post-acquisition integration risks in a maturing aesthetics market projected to cool after years of explosive growth driven by consumer demand for non-surgical enhancements. Looking ahead, sustained revenue gains hinge on cost controls and diversified pipelines, but persistent margin erosion could pressure stock performance and strategic pivots.

In the wider context, it reflects China's push for healthcare efficiency—centralized tenders have cut drug prices by up to 50% in recent years—potentially reshaping biopharma dynamics and favoring innovators over incumbents reliant on legacy assets.