Bosnia and Herzegovina has been placed on the Financial Action Task Force's increased monitoring list - commonly called the grey list - for deficiencies in its anti-money laundering and counter-terrorist financing framework. The designation does not signal a banking collapse, but it does create real friction for businesses and individuals conducting cross-border transactions. In response, the country's leading financial regulators moved quickly to contain the reputational damage with a coordinated public statement.

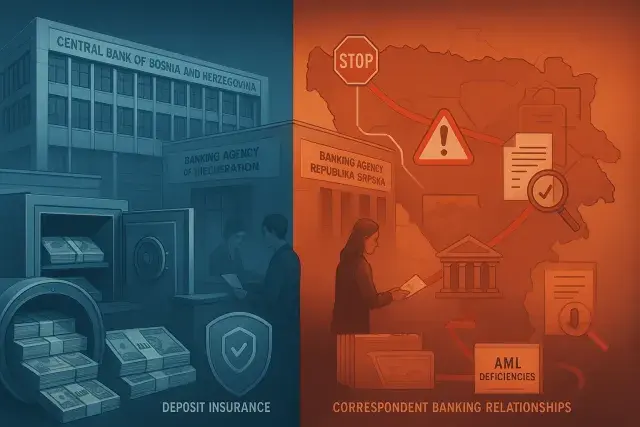

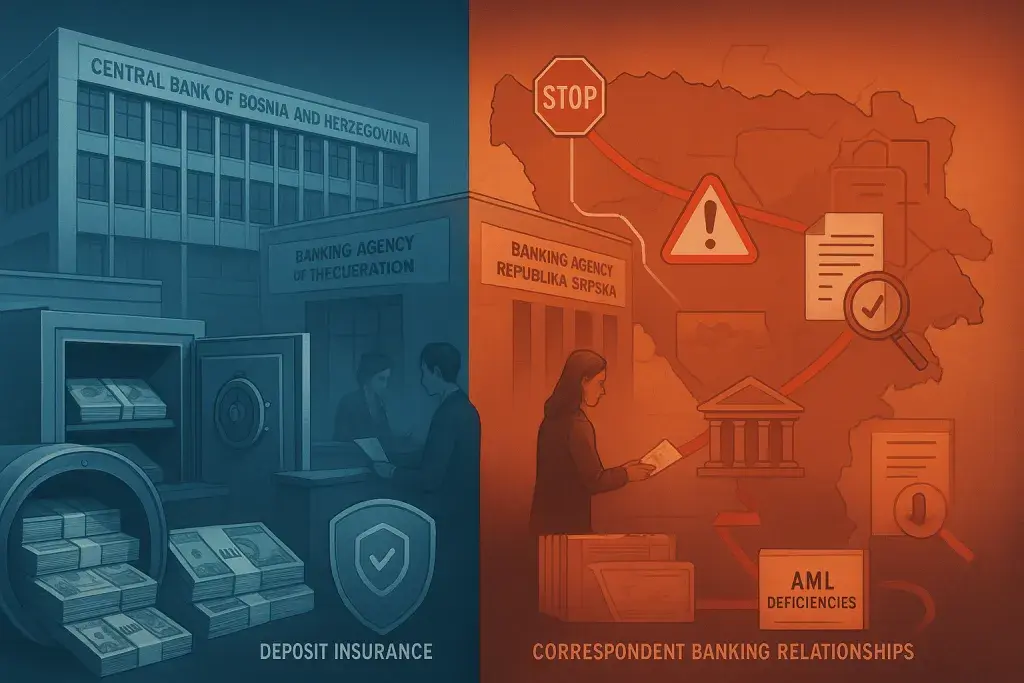

The joint communiqué comes from four institutions: the Central Bank of Bosnia and Herzegovina, the Deposit Insurance Agency, the Banking Agency of the Federation of Bosnia and Herzegovina, and the Banking Agency of Republika Srpska. Their core message is measured but deliberate - the domestic financial system is stable, liquid, adequately capitalized, and the convertible mark (BAM) remains firmly pegged to the euro through the currency board arrangement. What's striking here is how carefully the statement draws a line between the regulated banking sector, which the institutions say operates to international standards, and the broader institutional and legislative gaps that actually prompted the grey-list decision. Operators in other heavily regulated industries - including licensed cannabis retailers who rely on compliant payment infrastructure like cannabis POS for Nevada dispensaries - will recognize that pattern: financial regulators in scrutinized environments almost always separate systemic compliance from isolated policy failures, and for good reason.

The practical consequences, though, are worth reading carefully. Grey-list status does not freeze accounts or suspend correspondent banking relationships overnight. What it does is introduce friction at the international level - additional due diligence checks on cross-border transactions, longer processing windows, and higher administrative costs imposed by foreign and correspondent banks that are now required to apply enhanced scrutiny to counterparties in listed jurisdictions. That last point matters most for businesses that depend on efficient international payments: importers, exporters, and any enterprise whose supply chain crosses a border. The domestic payment system, the institutions emphasize, continues to function without interruption.

Why the Banking Sector Is Not the Source of the Problem

This is where the joint statement makes its most pointed argument. Bosnia and Herzegovina's banks, the four institutions state, already implement rigorous client identification, transaction monitoring, risk assessments, and mandatory reporting to competent bodies. In other words, the AML deficiency is upstream - in legislation and institutional coordination across the country's complex governance structure - not inside the banks themselves. That distinction matters because market reaction to grey-list designations often conflates regulatory gaps with sector-wide instability. The statement pushes back on exactly that conflation.

To put it plainly: a country can have a well-run, compliant banking sector operating within a broader legislative environment that hasn't yet met international AML benchmarks. The two conditions coexist more often than observers outside the field expect. The FATF process is specifically designed to address national-level framework gaps, not to rate individual financial institutions. What happens next depends heavily on how quickly competent authorities at all governance levels in Bosnia and Herzegovina can legislate and implement the required reforms.

The Real Operational Risk Is in International Transactions

For businesses and citizens, the friction will surface unevenly. Domestic transactions - payroll, retail purchases, utility payments, local supplier invoices - are unaffected. The pressure concentrates on cross-border activity: international wire transfers, trade finance, foreign correspondent relationships, and any payment that routes through a bank in a jurisdiction that applies enhanced due diligence to grey-listed countries. Expect longer processing times on certain transfers, requests for additional documentation, and in some cases increased fees passed through by correspondent banks covering their own compliance costs.

The institutions are transparent about this. They acknowledge that although the financial sector is not responsible for the underlying situation, it could bear the brunt of the practical effects internationally. That is an unusually candid admission from a regulatory body, and it signals that the institutions are preparing the market for a period of elevated operational cost rather than pretending the designation carries no consequences.

What Stability Guarantees Actually Cover - and What They Don't

The deposit insurance system, the statement confirms, continues to function and fully covers deposits held by individuals and legal entities in accordance with applicable regulations. The currency board arrangement - the mechanism that keeps the BAM pegged to the euro at a fixed rate - remains intact. These are meaningful assurances. Currency board systems are structurally conservative; they require full foreign-currency backing for the monetary base, which limits the central bank's discretion but also insulates the exchange rate from speculative pressure.

What stability guarantees cannot cover is the administrative burden that grey-list status places on businesses conducting international commerce. That burden is real, and it will likely persist until Bosnia and Herzegovina completes the legislative and institutional actions required to exit the monitoring list. The four institutions say they will act in a coordinated and responsible manner to preserve financial stability and strengthen confidence in the system. The coordination part is the hard variable - Bosnia and Herzegovina's governance structure requires alignment across multiple levels of authority, and that process takes time.

The takeaway for any business with cross-border exposure is straightforward: plan for additional documentation requirements, build in longer clearing windows on international transfers, and review correspondent banking relationships proactively. The domestic system holds. The international friction, however, is not a short-term anomaly - it is the practical cost of the designation until reform is complete.