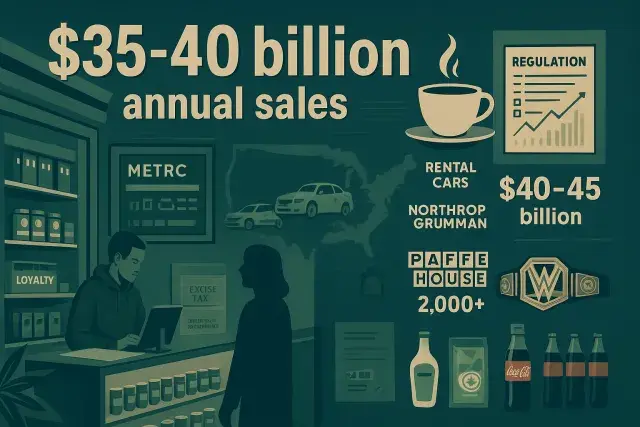

The U.S. legal cannabis market generates somewhere between $35 billion and $40 billion in annual sales - depending on whether medical and adult-use figures are counted together - placing it squarely alongside industries Americans rarely associate with a product that was federally prohibited not long ago. That comparison deserves more than a footnote. It has direct implications for how dispensary operators, multi-state operators, investors, and B2B suppliers think about the long-term trajectory of this business.

Put the numbers in context and the picture sharpens quickly. Specialty coffee generates comparable annual revenues by turning a daily ritual into a premium consumer experience - a pattern cannabis retail has been replicating with branded product lines, loyalty programs, and carefully designed budroom environments. The rental car sector, with its major national brands, produces annual revenues in roughly the same range, built entirely on consumer demand, regional economics, and regulatory variation by jurisdiction. Defense contractors such as Northrop Grumman and General Dynamics each post annual revenues in the $40 billion to $45 billion range - companies with federal contracts, decades of infrastructure, and deep institutional capital. Cannabis operators, by contrast, are building comparable economic volume while managing state-by-state licensing, seed-to-sale tracking requirements, 280E tax exposure that denies standard federal business deductions, and a persistent lack of access to conventional banking. For operators in newer markets - including those working with platforms like IndicaOnline Rhode Island to manage point-of-sale compliance and inventory in recently legalized states - the operational complexity behind that revenue figure is not abstract. It shows up every day in compliance logs, excise tax calculations, and METRC reporting.

The comparisons at the lower end of the scale are just as instructive. UFC and WWE, individually strong media and entertainment businesses, each clear well over $1 billion annually - yet combined they represent a fraction of legal cannabis revenue. Waffle House, one of America's most enduring restaurant brands with more than 2,000 locations across 25 states, generates an estimated $2 billion in annual sales. Ranch dressing - genuinely America's best-selling salad dressing - exceeds $1 billion at retail. These are not obscure benchmarks. They are household names with loyal consumers, established distribution networks, and decades of brand equity. Legal cannabis has already surpassed them. What's striking here is that cannabis accomplished this while operating under restrictions that none of those industries face: no interstate commerce, no federal banking access in most cases, no standard advertising channels in most regulated states, and tax treatment under 280E that can consume a disproportionate share of gross income at the operator level.

What the Revenue Scale Actually Means for Operators

Industry-wide revenue figures can obscure the structural pressures that individual operators feel at the store level. A dispensary generating strong gross sales still faces an effective tax burden that can run significantly higher than comparable retail businesses, because 280E prevents cannabis companies from deducting standard cost-of-goods and operating expenses at the federal level. Wholesale pricing compression - a persistent feature of maturing state markets - squeezes margins further. Compliant packaging mandates, mandatory lab testing with certificates of analysis on every product batch, SKU management across a growing product catalog, and state-mandated inventory reconciliation all add operational cost that a coffee chain or car rental desk simply does not carry.

The soft drink industry, which generates tens of billions annually through brands built on consumer loyalty and retail distribution, offers a useful structural parallel - but also a clear contrast. Coca-Cola and its peers move product across state lines freely, advertise nationally, access capital markets without restriction, and carry no compliance overhead resembling what a licensed cannabis retailer manages daily. That gap in structural advantage is part of why industry observers continue to watch federal regulatory developments closely. Any shift in 280E treatment, banking access under something like the SAFE Banking Act, or rescheduling under the Controlled Substances Act would not just affect cannabis companies symbolically - it would alter the fundamental unit economics of every licensed operator in every adult-use and medical market in the country.

Growth Trajectory and the States Still Coming Online

Unlike specialty coffee or rental cars - mature categories growing modestly - cannabis is still adding entire state markets. Each new adult-use legalization brings a new taxable retail base, a new wave of licensed operators, new wholesale demand, and new compliance infrastructure requirements. Analysts broadly expect the market to continue expanding through the remainder of the decade, with the pace depending in part on how many additional states move from medical-only programs to full adult-use frameworks, and whether federal action reduces the structural friction that currently limits growth.

For B2B suppliers - point-of-sale software vendors, seed-to-sale compliance technology providers, cannabis-friendly payment processors, packaging manufacturers, testing laboratories, and real estate operators serving the licensed trade - that trajectory matters. The addressable market for cannabis B2B services scales with the number of licensed retail locations and cultivation facilities operating in compliant markets. More states, more licenses, more operators means more demand for the infrastructure layer that keeps regulated cannabis retail running. In practice, though, that growth is not automatic or frictionless. New markets launch with regulatory uncertainty, licensing backlogs, social equity program complexities, and local zoning restrictions that can delay store openings for months or years after a state's law takes effect.

The Industry's Economic Weight Demands Serious Business Treatment

Cannabis has earned comparison to defense contractors and national restaurant chains not through favorable press coverage but through transaction volume, employment, and tax contributions across dozens of state economies. That economic weight carries a straightforward implication for everyone operating in or adjacent to this market: this is not a niche category waiting to be legitimized. It is a large, complex, highly regulated industry with the compliance burden of pharmaceuticals, the consumer dynamics of packaged goods retail, and the capital constraints of a business sector still denied full access to the U.S. banking system.

Operators, investors, and suppliers who treat it accordingly - building genuine compliance infrastructure, investing in technology that handles regulatory reporting accurately, managing supply chain and inventory with the discipline that seed-to-sale requirements demand - are positioned differently than those still running cannabis retail like an informal operation that happened to get licensed. The revenue comparisons are real. So are the operational requirements attached to them.